Healthy, Wealthy and Wise

From Issue #1:

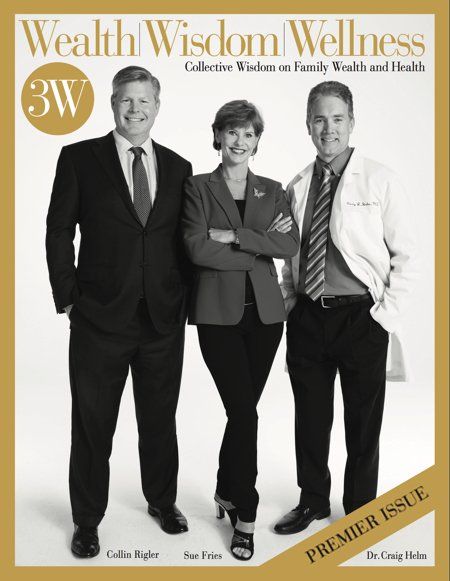

Collin Rigler, Wealth Manager with a Competitive Advantage

Collin Rigler, Senior Vice President at RBC Wealth Management is an extremely successful and confident wealth manager. And he has good reason to be. Collin majored in applied economics, helped take companies public, consults with colleagues that work in the Federal Reserve and has an impressive list of CEO and executive clients in a wide range of industries. But that’s not all.

While Collin’s credentials rank in the top of his field, he has an ace up his sleeve; a competitive advantage over most wealth managers. When Collin was managing institutional portfolios, he learned directly from William O’Neil + Co, the data analysis and investing style of its founder, William O’Neil. O’Neil founded Investor’s Business Daily and William O’Neil + Co. which provides investment analysis to top hedge funds and mutual fund managers.

For someone who is sought after by power movers in many industries, we found Collin to be quite humble. No doubt he is confident in what he does, he has real passion for keeping on top of his game in the ever-changing markets. He considers it an honor to be fortunate enough to use his talents to help many families grow their wealth and legacy.

We spent some time with Collin and talked about how he might help families in Valencia.

3W: Collin let’s talk about Valencia specifically the Westridge, Stevenson Ranch Woodlands and surrounding areas.

Collin: I’m familiar with those areas. There are many hard-working families, intelligent successful folks, nice homes and good schools too.

3W: What are common mistakes that the intelligent investor should look out for?

Collin: Not selling! In my opinion, holding onto last year’s losers is a very costly mistake. More people have lost money because they fall in love with a sector or a stock that has become like their pet which they never want to sell. Not selling losers and redirecting that money into something more productive is a mistake that everybody makes.

3W: What do you do differently for your clients?

Collin: We manage our client’s money on a proactive basis so we’re ready to buy into the market when there is opportunity to make money for you and get you out to minimize any loss. We do what you’re currently paying your financial advisor to do but may not be getting.

3W: Financial Advisors tend to put folks in mutual funds; kind of set it and forget it. Is that a good idea?

Collin: If you just want to own mutual funds, there are many very good and competent managers. 99% of mutual funds are what we call “long only”, where they’re picking what they think are the best stocks in their sector or industry group. But what that 99% of mutual fund managers won’t do is get you out in times of trouble. So clearly just owning mutual funds is not really a total “investment strategy.”

3W: Then what should we have in our portfolio?

Collin: You need something in your portfolio that has the ability to out-perform when the market goes down; you need some type of mechanism where you’re going to cash, and another mechanism knowing when the appropriate time is to buy back in. If you don’t have those you might as well just buy the S&P 500 and call it a day because you’re just paying management fees.

3W: So you’re on top of your client’s portfolios on a daily basis, what indicators and methods do you use?

Collin: We analyze data from 3,000 money managers in the country and we ask them if they’re bullish, bearish, or neutral. We look at the percentage difference between advisors who are bullish and those who are bearish. If there are too many bearish managers we know the market may be bottoming. If there are too many bullish managers we know the market may be topping. We look for readings that have been very consistent over time before we take action.

3W: What else do you research for market indicators?

Collin: Generally, we look at market direction, technical indicators (such as the 200-Day Moving Average), and we look at some tactical indicators. However, the psychological indicators are probably one of the best indicators you’re ever going to have in the market.

In addition, there’s a system where we screen for current and annual earnings per share, new products, services or new management in the company; we look at some type of catalyst or trigger that we think is going to make the stock go up, and we also want to make sure it’s a leader in the industry.

3W: In layman’s terms?

Collin: We want to be invested in the leaders of an industry because there’s a reason they’re a leader. We want to be in companies that are big enough, that have institutional sponsorships where mutual funds and hedge funds are buying these companies aggressively; that’s really the fuel that makes stocks go up. But in the final analysis, none of this works unless the market is going in the right direction.

3W: Is it possible for a novice to just copy what the institutional investors are buying?

Collin: The market is very volatile, so you need to know what you’re doing, which is why we have strict risk controls on the downside of our portfolios.

3W: Tell me about William O’Neil, founder of William O’Neil + Co. and Investor’s Business Daily.

Collin: William O’Neil took certain criteria and statistics and figured out which stocks were the best out-performers every year, and what characteristics they had in common. From that he developed a system that became so successful he made enough money to buy his own seat on the NYSE. Hedge funds and money managers use his consulting services to evaluate their portfolios. He tells them what they’re doing right or wrong from an individual stock basis all the way to which industry groups they own. Managers pay a lot of money to gain access to his knowledge.

3W: What advice would you give to those who love learning and investing on their own versus giving you a chunk of their earned income to invest?

Collin: I would say that investing on your own is very difficult, and you need a very good understanding of economics, finance and human psychology. Once you acquire that basic knowledge and understanding you really must have experience. Doing things repeatedly with the right skill set is the only way you can attain that status, especially as it relates to the stock market. You need to invest a lot of time, effort, hard knocks, loses and realize it’s a very long learning process.

3W: Should investors still follow the Modern Portfolio Theory (MPT) of reducing risk by diversification, or is that theory even relevant anymore, and why?

Collin: MPT may work if you’re IBM Pension Fund or State Pension Fund of California, because you can take these numbers, you can diversify, and you’re going to own that portfolio over several market cycles. You’re going to need to give your pensioners a payout over time – 20, 30, 40 years from now.

For an individual investor, I’ve found the time frame is usually 3 to 5 years, no matter how wealthy you are. Things change, you may buy a new house, or an airplane or business, get divorced, send kids to college, so your timeframe is much shorter. Therefore, you cannot afford to have these large drawdowns like we saw in 2001 and 2008 and still hope to retire, pay your kid’s way through college and maintain your lifestyle. You need something different than MPT that is not only going to diversify you, but is going to give you the opportunity to buy quality companies at lower prices and get you out of portions of the market when it starts to go south.

3W: What’s your advice on how to avoid the pitfalls of what could potentially become a very volatile stock market in the next few years?

Collin: If we do get into a real ugly market like we did in 2001 or 2008, we have some very strategic options. Most traditional portfolios are counting on the fact that diversification will save you, but we all know that in times of a financial crisis the direction of most of these asset classes is down. When our technical and psychological indicators get to extremes, we have the ability to be in cash. We also have a portion of the portfolio that is constructed to outperform in down markets. And, contrary to what people think, we are going to be a long-term owner of blue chip companies even in down markets. We want to hold those stocks, collect the dividends and reinvest them at lower prices. That is how you get long-term outperformance over market cycles.

3W: Let’s talk about the Federal Reserve. Does the Fed have any shelf life left?

Collin: I studied economics in college, many of my classmates now work at the fed or have worked closely with the Federal Reserve for years. I believe I have a very good idea what they are attempting to do and what their exit strategies may be after QE. The market has clearly been driven by Fed policy recently and that is why index investing has become so prevalent. As the economy grows and rates rise there will be winners and losers in the financial markets, movements will be based more on fundamentals and economic growth than cheap money. Fed policy will always be important to the markets but I think monetary policy will take a backseat to fiscal policy and good old fashioned fundamentals going forward. A proactive investment approach is going to be more appropriate than just sitting in an index in that environment. Going forward, no one knows exactly what is going to happen with Fed policy, even Janet Yellen. I think what they’re going to do is called yield curve management. I think eventually if this economy starts overheating they’re going to start selling the bond portfolio, which will raise long term rates and stop inflation in its tracks; but it will keep the yield curve steep so we still have growth.

3W: If our readers are interested in what you might do for their portfolio how should they contact you?

Collin: I’m a family man just like them. Please have them call me at 310-647-8041 or they can email me. I love to talk about the markets with people who are interested. If you already have an advisor I’m happy to take a look and give you a second opinion. You may have started investing years ago and all you have been doing is rebalancing every year. That might not be the best portfolio for you. That is why we rebalance to the current market indicators and your unique situation. Also, they can simply call or email us and we can provide them with a weekly market recap and/or timely investment ideas.

Past performance is not indicative of future results. This material is for informational purposes only, and not intended to replace the advice of a qualified tax advisor, attorney, accountant or financial advisor.

Collin Rigler

Managing Director – Client Advisor

ALEX BROWN

10250 Constellation Blvd. Suite 850

Los Angeles, CA90067

424-303-6403

Collin.rigler@alexbrown.com

VIEW MORE ARTICLES BY ISSUE: